Independent Board Advisory, Executive Education and Professional Speaking

New Success Metrics Beyond TSR

The Singapore Institute of Directors first published my article "New Success Metrics Beyond TSR" in the Q3 2026 issue of the SID Directors Bulletin.

Lee Ooi Keong

6/29/20266 min read

New Success Metrics Beyond TSR

SID Directors Bulletin - Q3 2026: Future Forward

Boards have long leaned on total shareholder return (TSR) as a shorthand for performance. In today’s environment of heightened stakeholder scrutiny, regulatory complexity and long-term strategic risk, accountability must pivot toward a broader, more deliberate framework. This means embedding oversight mechanisms that track not only financial outcomes but also operational resilience, risk management discipline, ethical conduct and stakeholder trust.

Rather than relying on a single market-based signal, boards can draw on a set of validated, evidence-based frameworks that assess governance quality through the behaviours, processes and decision-making rigour that drive long-term organisational effectiveness. These frameworks shift the basis of evaluation from financial outcomes, which boards do not fully control, to the governance inputs and conduct that they do.

Today, TSR dominates board performance evaluation globally, appearing in over 60 per cent of long-term incentive plans. Often regarded as the gold standard, TSR proffers the ultimate measure of board success. The appeal is obvious: one number linking board performance to shareholder returns.

The formula appears simple: ending stock price minus initial price plus dividends. Yet, this simplicity masks fundamental flaws that render TSR inadequate for measuring board effectiveness. Research shows that these limitations create significant governance blind spots.

Just as compliance alone cannot ensure board effectiveness, the critical question is whether existing metrics actually measure governance quality or merely document processes.

The TSR challenge

The key limitations of using TRS as a performance benchmark are:

Limited visibility into operational drivers like return on capital or innovation investments.

External factors beyond the board’s control significantly influence outcomes, including interest rates, GDP growth, commodity prices, and geopolitical events.

TSR lags operational performance. Research and development and innovation investments often take years to be reflected in share prices.

Research validates these concerns. Some examples are:

Pearl Meyer and Cornell University’s decade-long S&P 500 analysis found zero statistical relationship between TSR-based incentive plans and improved financial performance. Worse, companies using TSR plans underperformed peers on revenue growth and profitability.

BCG research demonstrates that earnings growth drives only 25 per cent of TSR movements while revenue growth accounts for just 15 per cent. Market forces drive the remaining 60 per cent. This creates “pay-for-luck” scenarios in which boards are rewarded for market volatility rather than for governance quality.

Harvard research confirms that TSR lacks two critical measurement elements: clear line of sight linking board actions to outcomes and actionable improvement information.

Historical examples prove the point. For example, Enron's stock rose 87 per cent in 2000, reaching US$90.75 (S$115.50), then collapsed to US$0.26 within 15 months. WorldCom maintained a US$64 share price while perpetrating a US$11 billion accounting fraud. Wells Fargo traded above US$50 through mid-2016 before fake account scandals triggered sustained declines.

In each case, strong TSR masked governance failures that traditional metrics missed.

Compliance vs effectiveness

Singapore boards face clear expectations with the Code of Corporate Governance by the Monetary Authority of Singapore (MAS), which operates under a “comply-or-explain” regime. The Code establishes governance foundations and consistent standards, though process compliance may not automatically translate to board effectiveness.

The Singapore Governance and Transparency Index (SGTI) assesses all Singapore companies based on public disclosures. However, recent examples show companies with strong SGTI scores still faced governance crises, highlighting the gap between scores and actual effectiveness.

The evidence suggests external assessments capture documentation quality rather than decision-making effectiveness.

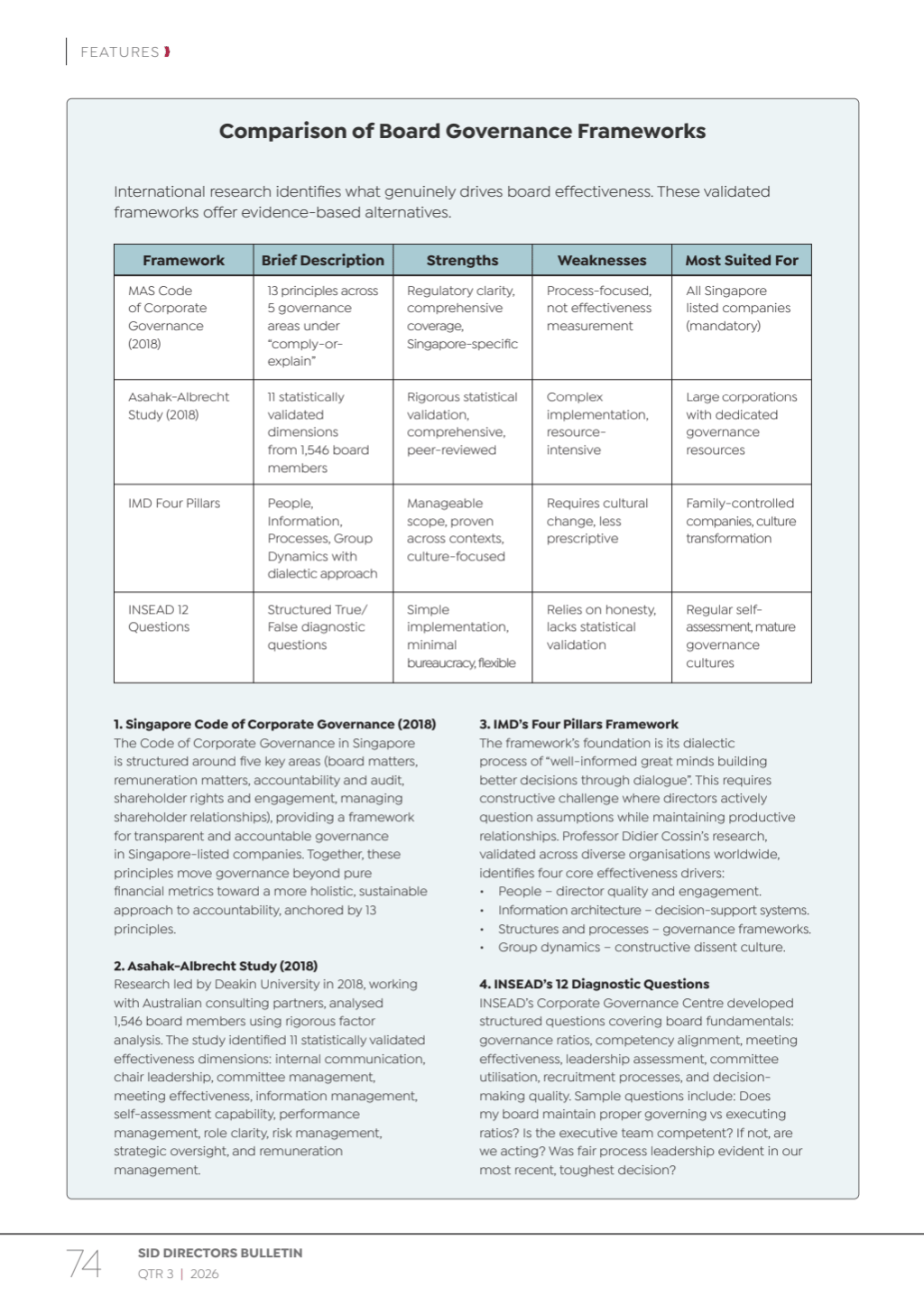

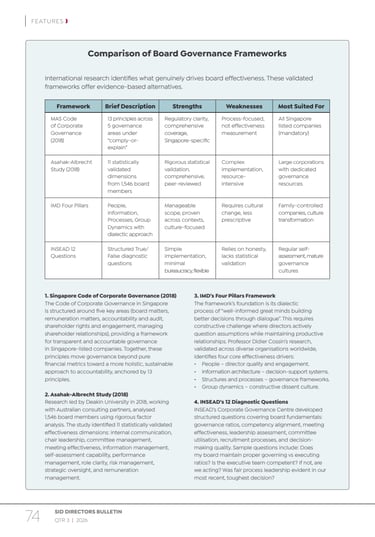

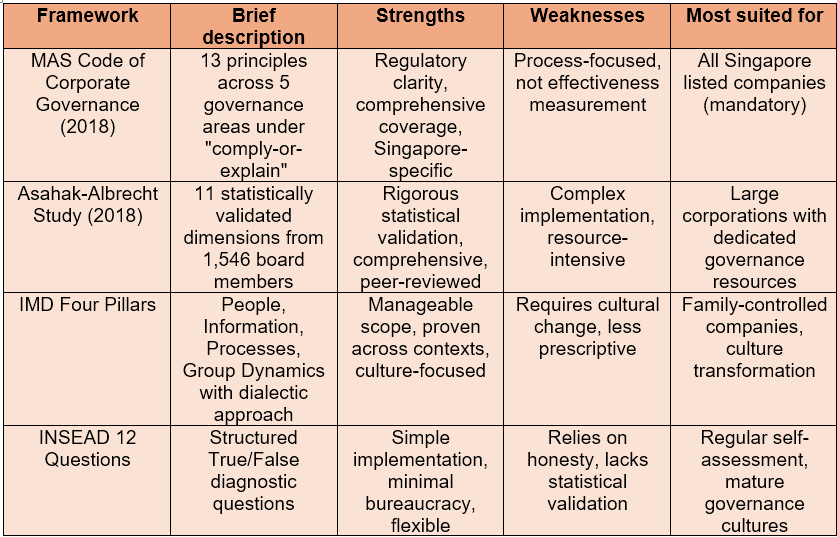

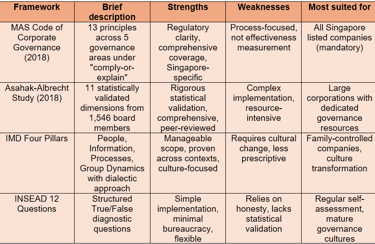

Comparison of Board Governance Frameworks

International research identifies what genuinely drives board effectiveness. These validated frameworks offer evidence-based alternatives.

1. Singapore Code of Corporate Governance (2018)

The Code of Corporate Governance in Singapore is structured around five key areas (Board matters, remuneration matters, accountability and audit, shareholder rights and engagement, managing shareholder relationships), providing a framework for transparent and accountable governance in Singapore-listed companies. Together, these principles move governance beyond pure financial metrics toward a more holistic, sustainable approach to accountability, anchored by 13 principles.

2. Asahak-Albrecht Study (2018)

Research led by Deakin University in 2018, working with Australian consulting partners, analysed 1,546 board members using rigorous factor analysis. The study identified 11 statistically validated effectiveness dimensions: internal communication, chair leadership, committee management, meeting effectiveness, information management, self-assessment capability, performance management, role clarity, risk management, strategic oversight, and remuneration management.

3. IMD's Four Pillars Framework

The framework's foundation is its dialectic process of “well-informed great minds building better decisions through dialogue”. This requires constructive challenge where directors actively question assumptions while maintaining productive relationships. Professor Didier Cossin's research, validated across diverse organisations worldwide, identifies four core effectiveness drivers:

People – director quality and engagement.

Information architecture – decision-support systems.

Structures and processes – governance frameworks.

Group dynamics – constructive dissent culture.

4. INSEAD's 12 Diagnostic Questions

INSEAD's Corporate Governance Centre developed structured questions covering board fundamentals: governance ratios, competency alignment, meeting effectiveness, leadership assessment, committee utilisation, recruitment processes, and decision-making quality. Sample questions include: Does my board maintain proper governing vs executing ratios? Is the executive team competent? If not, are we acting? Was fair process leadership evident in our most recent, toughest decision?

Using the integration approach

Singapore boards face a practical challenge: multiple validated frameworks exist, but implementation capacity varies significantly. Rather than adopting all approaches simultaneously, boards should select based on specific criteria.

Consider governance maturity first. Boards comfortable with challenging conversations can handle comprehensive frameworks like Asahak-Albrecht's eleven dimensions. Boards preferring gradual development benefit from IMD's four pillars or INSEAD's diagnostic questions.

Match organisational context. Family-controlled companies (common in Singapore) often benefit from IMD's emphasis on constructive dissent and group dynamics. Large corporations may prefer Asahak-Albrecht's systematic approach. Boards seeking immediate implementation favour INSEAD's question-based method.

Assess implementation capacity honestly. Asahak-Albrecht requires systematic evaluation across eleven dimensions. IMD needs cultural transformation support. INSEAD demands facilitation skills and honest dialogue among directors.

Singapore boards can enhance existing processes through research insights rather than creating parallel systems. Considerations should include the following guidelines.

Focus on research-proven governance behaviours. Ask uncomfortable questions, challenge management assumptions, ensure dissenting views receive consideration, and make difficult decisions despite incomplete information. These behaviours create effective governance regardless of the specific measurement system.

Implement quarterly discussions. Use framework-guided conversations. Ask: Are we genuinely challenging management recommendations? Do dissenting views feel safe to emerge?" "Are we making decisions or approving predetermined outcomes? These questions reveal governance quality better than compliance checklists.

Engage external perspectives. Assess governance culture and decision-making processes rather than compliance documentation. Use independent observations to calibrate self-assessment accuracy and identify improvement areas.

Singapore can demonstrate regional governance leadership by showing how to enhance regulatory compliance through evidence-based effectiveness measurement. The MAS Code provides solid regulatory foundations. The opportunity lies in using compliance requirements as minimum standards rather than maximum achievements.

Research consistently shows that effective governance stems from specific behaviours and processes that are difficult to quantify but can be systematically developed. Boards that focus on these behaviours (constructive challenge, information quality, decision-making processes) significantly outperform those that focus solely on scoring systems.

Recent global governance challenges prove that measurement systems cannot substitute for engaged stewardship. Directors who navigate future challenges successfully will focus on governance behaviours that research validates rather than metrics that markets celebrate.

The path forward

Singapore directors face an immediate choice. Continue measuring what is easy to document or start developing what actually drives board effectiveness.

The research is clear. The frameworks are validated. The regulatory environment supports innovation. What is missing is the courage to prioritise substance over appearance.

Board assessment should start with the following:

First, select one evidence-based framework that fits your board's maturity and context. Don't try to implement everything simultaneously.

Second, integrate effectiveness questions into existing processes rather than creating new bureaucracy. Transform routine compliance discussions into governance development conversations.

Third, commit to an annual honest assessment of governance behaviours, not just compliance scores. Ask the uncomfortable questions that reveal actual board quality.

Singapore’s governance leadership begins with boards that choose effectiveness over scores, development over documentation, and behavioural change over measurement theatre.

Your next board meeting is where transformation starts.

By Lee Ooi Keong, Independent Director, Info-Tech Systems